Subscribe and receive email notifications of new blog posts.

RSS Feed

RSS Feed

7

Not a State of The Union, Just A Rambling Of Numbers

There are a lot of numbers and statistics that can tell us where we are in the real estate world today. Trying to find out where we are headed is another thing. In this article, Inflation Gauge Eases, Raising Chance of Rate Cut by Christopher Rugaber, he states:

"Prices rose just 0.1% from July to August, the Commerce Department said, down from the previous month's 0.2% increase. Compared with a year earlier, inflation fell to 2.2%, down from 2.5% the previous month and barely above the Fed's 2% inflation target . . . Compared with 12 months earlier, core prices rose 2.7% in August, slightly higher than in July. With inflation having tumbled from its 2022 peak to barely above the Fed's 2% target, the central bank last week cut its benchmark interest rate by an unusually large half-point, a dramatic shift after more than two years of high rates. The policymakers also signaled that they expect to reduce their key rate by an additional half-point in November and in December. And they envision four more rate cuts in 2025 and two in 2026."

This is the news that we've been wanting to hear for the last few years, that policymakers are signaling approximately 8 more rate reductions between now and the end of 2026. Let's assume that these 8 cuts are small, say .25%. That would mean that we may see an additional drop of 2 full percentage points with the Federal Funds rate in the next 1 ½ years.

As you know by definition, "The federal funds rate is the interest rate at which banks lend money to each other overnight. It's a key benchmark rate that affects other interest rates, like those for mortgages, credit cards, and auto loans." The current Federal Funds rate is 4.75% - 5.0%. If we actually see the predicted 2% drop over the next 1 ½ years, the rate range would drop to 2.75% - 3.0%. Unfortunately, mortgage rates do not follow the Federal Funds rate directly. "My best guess is that the average 30-year fixed mortgage rate will be around 5.5% a year from now," said Ted Rossman, senior industry analyst for CreditCards.com and Bankrate.com" from This USA Today Article. If the Federal Funds rate trend prediction above is accurate, a year from now the rate range would be about 3.5% - 3.75%. But, an average of 5.5% for mortgage rates may move the consumer discussions away from "high rates" (please remember, in Fall 2023 a 7.5% mortgage rate was not unheard of).

So regarding mortgage rates, our market should be optimistic the next few years, although we still have other headwinds. The unprecedented low rates of 2011 – 2020 were great, but they contributed to pushing real estate prices up considerably. This was good news for owners of real estate, but actually bad news for younger consumers trying to participate in the American Dream. 10 years ago, according to our Baldwin MLS, the average sale price of a Residential Detached home in 2014 was $204,637. Year to date in 2024, the average sale price of a Residential Detached home is $429,820 – a 110% increase! I don't think wages have increased 110% in the past 10 years, challenging our real estate affordability.

The good news is that consumers are still showing strength and able to keep purchasing, even though at a slower pace than we have experienced in the last few years. According to BR MLS, year to date, there were 5097 residential sales in 2024 vs. 3111 YTD 2014 – a 64% increase in the number of residential transactions compared to 10 years ago . . . and this is in what we are calling a slow market. A lot of these consumers have come from other areas, as the Baldwin County population in 2014 was 199,306 versus an estimate in 2024 of 260,483 according to the most recent United States census data – a 31% population increase in 10 years. Compare that to the population growth of the US – 318.4 million in 2014 vs 345.9 million in 2024 = 8.6% growth. 31% vs 8.6% - even if the national economy is not robust, one would think that the Baldwin County population growth would continue to keep our local economies performing better than the nation.

As I write this, I cannot help but feel the Insurance Albatross on my back. This may be the biggest drag on our coastal real estate economy going forward. I could not find any statistics that made any comparative sense, but we all know that insurance cost is WAY UP! We hear nightmare stories about condominium assessments as a result of condo hazard insurance doubling and tripling since Hurricane Sally came to visit. Pile on top of that the structural improvement requirements that are catching up to our older condo buildings, and the cost of ownership of these investments is wreaking havoc on the ROI. I remember about 20 years back when rental rates were not very high, and buyers would enter the market thinking they could find a condo that would cashflow even with a 75% mortgage . . . and it was virtually impossible to find one. We were trained to tell these buyers to consider the rental income as just a "dividend", that the condo would not "pay for itself". The condo market got spoiled with the appreciation we have had since then, and even though the rentals would still not "pay for itself", the appreciation sure made it worthwhile to be a condo owner. Who knows where condo pricing is headed today, but with 1057 condos on the market in Gulf Shores and Orange Beach (as of this first week in October), my feeling is that we have peaked for a while.

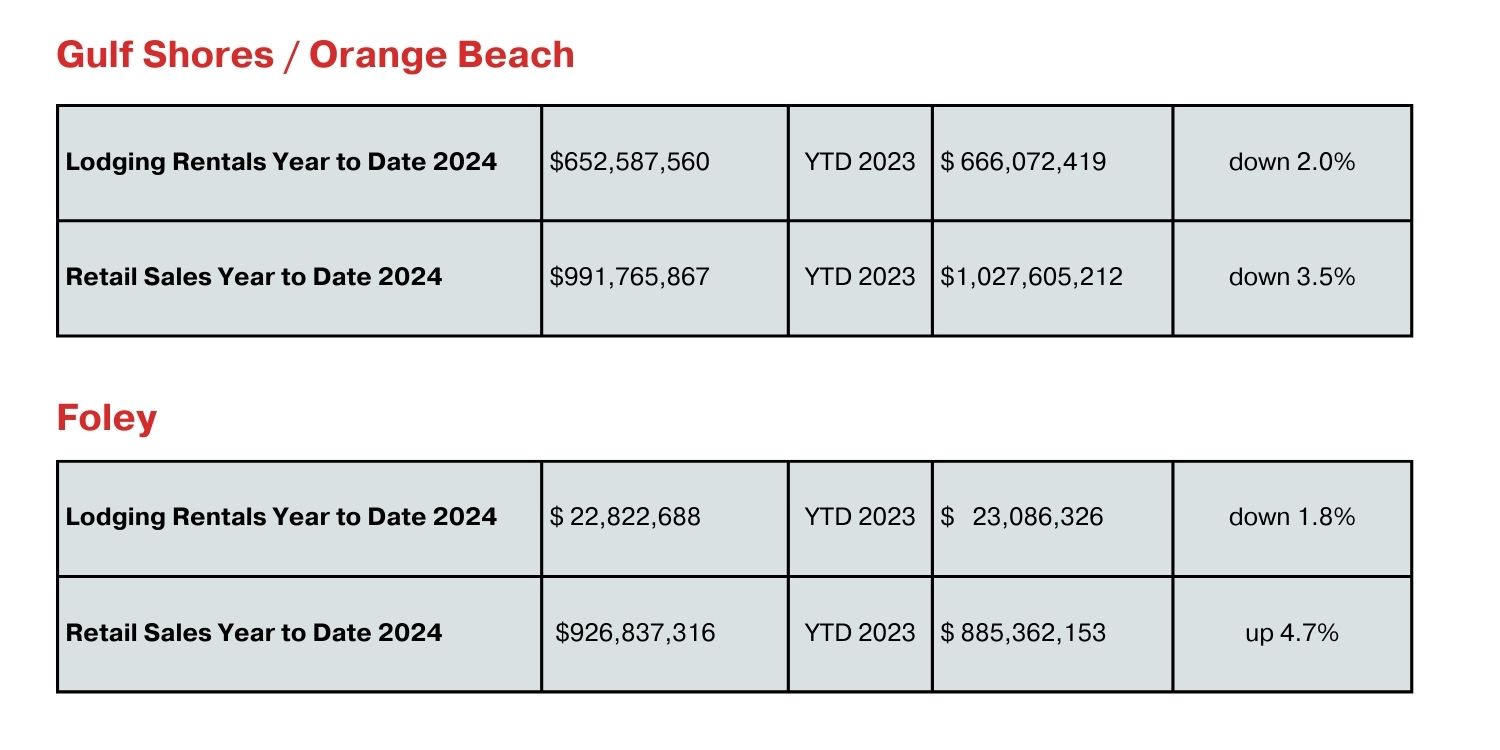

Want to see some other interesting numbers? How about this:

Dang - Foley retail sales are almost equal to Gulf Shores and Orange Beach combined!! I guess you may have figured that if you have driven through there recently.

So, there you have it. What does all this rambling mean? Hell, if I know!

Social